addressing any of the specific, substantive problems and questions with these numbers that oldr and I have raised...just more misleading blather, more delusional triumphalism, and some sideshow info that's irrelevant to issues that have been raised...

Who's Sorry Now?

Re: Who's Sorry Now?

Yet another rah-rah post and still not a word:

Re: Who's Sorry Now?

Those two red dots are the taillights of the ACA program disappearing away from you over the horizon. You've missed the bus again. :

One should try to have a sense of perspective about what the numbers are and what they mean. I have no time to waste with people who don't.

http://acasignups.net/

yrs,

rubato

If you have questions then you should try to answer them. I'm not wasting time with the same ignorant bullshit tactic used by the tobacco companies and by the anti-global warming forces again.Submitted by Olav Grinde on Tue, 01/14/2014 - 8:29am

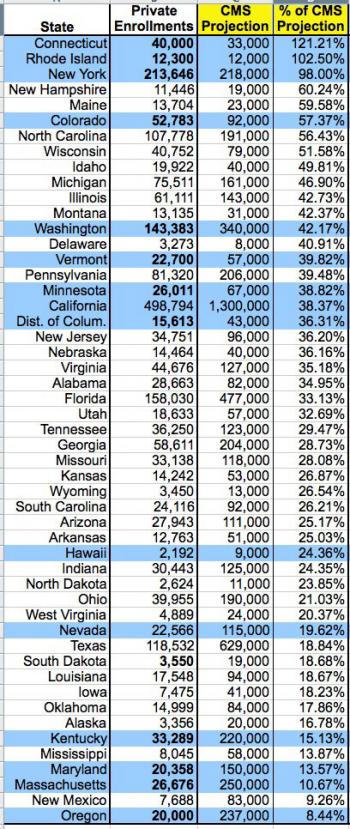

Yesterday, Charles Gaba examined the big numbers in the most recent HHS report, an unanswered question in the Medicaid numbers and sorted states according to how they’re doing relative to their (admittedly debatable) enrollment targets. Here I would like to briefly mention some rather interesting outliers and other data points, and share a few observations.

There is an 8 % difference between the genders: 54 % of those who have selected a Marketplace plan are women, while men account for only 46 %. Men are in the majority in only two states: Connecticut (54 %) and Hawaii (51 %), whereas the District of Columbia was evenly split per 12/28.

It’s also worth noting that in the District of Columbia, so-called “young invincibles” (enrollees between 18–34 years of age) account for 44 %, while in Massachusetts HHS pegs the portion to be 31 %. Nationally, people 34 years of age or younger account for 30 % of the enrollment, and 18–34 year olds account for just over 24 %.

One should try to have a sense of perspective about what the numbers are and what they mean. I have no time to waste with people who don't.

http://acasignups.net/

yrs,

rubato

Re: Who's Sorry Now?

We interrupt this non-stop propaganda monologue for a musical interlude...

Ladies and gentlemen, let's have a big Plan B welcome for...

The one, the only...

Miss Connie Francis!

Ladies and gentlemen, let's have a big Plan B welcome for...

The one, the only...

Miss Connie Francis!

Last edited by Lord Jim on Sat Jan 18, 2014 12:25 am, edited 5 times in total.

-

oldr_n_wsr

- Posts: 10838

- Joined: Sun Apr 18, 2010 1:59 am

Re: Who's Sorry Now?

Quite an accomplishment when the people who don't have health insurance are forced "by law" to sign up and those that had insurance you force their carriers to cancel those plans (as they were deemed not "good enough") so they too have to go shopping for new policies.

Yeah, those are good numbers

The mob used to do something similar to the neighborhood businesses.

Don't have protection?

Pay for protection or get

Already got protection (perhaps cheaper) from someone else?

That protection's not good enough so we are cancelling it.

Now pay (perhaps more) for our "better" protection or get

Yeah, those are good numbers

The mob used to do something similar to the neighborhood businesses.

Don't have protection?

Pay for protection or get

Already got protection (perhaps cheaper) from someone else?

That protection's not good enough so we are cancelling it.

Now pay (perhaps more) for our "better" protection or get

All the people who were perfectly fine with their old policies, all the people who didn't want to sign up, all the people who are paying higher premiums for their new policies......Who's Sorry Now?

Re: Who's Sorry Now?

I was trying to sit back and give Obamacare some time before deciding whether or not I like it. It's difficult for me to support it right now. One of many promises was that premiums for everyone would go down after people who previously weren't insured become insured.

As of 1/1/2014 my health insurance premium is twice the amount I paid in 2013.

When will my premium be reduced?

Should I hold my breath?

As of 1/1/2014 my health insurance premium is twice the amount I paid in 2013.

When will my premium be reduced?

Should I hold my breath?

Re: Who's Sorry Now?

Hold it long enough and you'll be paying nothing for healthcare!Joe Guy wrote:

Should I hold my breath?

“If you trust in yourself, and believe in your dreams, and follow your star. . . you'll still get beaten by people who spent their time working hard and learning things and weren't so lazy.”

Re: Who's Sorry Now?

To use a football analogy, anyone applying an ounce of objectivity who pays attention to what's going on with this, can see that the ACA is currently behind on the score board with third and long in it's own territory, and the clock running...

Not beat yet, but with a lot of ground to make up to pull out a victory...

Anyone that is, except for a delusional team water boy who's running around in the end zone doing a victory dance, as though the winning touchdown has already been scored, and it's time for fist pumping and high-fiving...

The disconnect is truly hilarious...

Not beat yet, but with a lot of ground to make up to pull out a victory...

Anyone that is, except for a delusional team water boy who's running around in the end zone doing a victory dance, as though the winning touchdown has already been scored, and it's time for fist pumping and high-fiving...

The disconnect is truly hilarious...

Re: Who's Sorry Now?

Well the numbers in Michigan are reportedly right where they were targeted to be at this point. Though they are on par with the national percentage of "invincibles" coming in at 25%

At this point things are looking up for the ACA and most analysts are ruling out the "Dismal Failure" outcome, but, there is still a lot of time (haven't even hit halftime yet) and a lot that can happen.

Personally I think it will end up a "meh" or better depending largely on how the "red states" shake out.

At this point things are looking up for the ACA and most analysts are ruling out the "Dismal Failure" outcome, but, there is still a lot of time (haven't even hit halftime yet) and a lot that can happen.

Personally I think it will end up a "meh" or better depending largely on how the "red states" shake out.

Okay... There's all kinds of things wrong with what you just said.

Re: Who's Sorry Now?

Another important factor is how many of the "enrollees" being counted in the figures actually pay and wind up as genuine "enrollees'; a breakdown that the Administration refuses to release...

As I pointed out in an earlier post, the latest numbers from Washington state on this showed about a 50-50 split...(that information was actually on the spread sheet that the water boy keeps trumpeting; funny he didn't make any mention of that...)

Presumably the drop off won't be 50%, but if 50 percent is representative of the current baseline, it's still going to be quite substantial...

Which would explain why the Administration won't release the national number; if it was something like 5% you better believe they'd be providing it...

Just like if the national percentage of "young and healthy" sign ups was anywhere near or above the target needed for the premium costs to work as advertised, they'd be trumpeting it rather than sitting on it...

As I pointed out in an earlier post, the latest numbers from Washington state on this showed about a 50-50 split...(that information was actually on the spread sheet that the water boy keeps trumpeting; funny he didn't make any mention of that...)

Presumably the drop off won't be 50%, but if 50 percent is representative of the current baseline, it's still going to be quite substantial...

Which would explain why the Administration won't release the national number; if it was something like 5% you better believe they'd be providing it...

Just like if the national percentage of "young and healthy" sign ups was anywhere near or above the target needed for the premium costs to work as advertised, they'd be trumpeting it rather than sitting on it...

Re: Who's Sorry Now?

The young and health is at about 25% from what I hear. Low but not cetastrophically low.

Okay... There's all kinds of things wrong with what you just said.

-

oldr_n_wsr

- Posts: 10838

- Joined: Sun Apr 18, 2010 1:59 am

Re: Who's Sorry Now?

http://www.fool.com/investing/general/2 ... -fail.aspxDoes This New Data Mean That Obamacare Will Fail?

By Sean Williams | More Articles | Save For Later

January 15, 2014 | Comments (29)

The past three-and-a-half months have been nothing short of a roller-coaster ride for Obamacare and its state and federally run health exchanges.

Opinions regarding the Patient Protection and Affordable Care Act have been bifurcated for years -- and enrollment results in October, November, and December have delivered in an equal, if not greater, bifurcation in their results.

October and November were absolutely marred by IT-source code glitches and overloaded servers, which caused the federally run website, Healthcare.gov, to be unusable for a majority of the citizens it services across 36 states. Through the first two months, federal sign-ups stood at just 137,204, placing them well short of initial sign-up estimates by the Department of Health and Human Services, which has been targeted 7 million paying enrollees by the March 31 coverage cutoff date for 2014.

In December, the tech surge, headed by the trio of Oracle, Red Hat, and Google, and overseen by UnitedHealth Group subsidiary, Quality Software Services, coupled with the Dec. 24 coverage cutoff deadline for Jan. 1, led to a surge in cumulative state and federal enrollments, from 364,682 through November to 2,153,421 people through Dec. 28. Other pertinent information from inception through Dec. 28 includes 53.2 million state and federal website visits and 11.3 million calls to state and federal call centers.

One pressing question finally answered

A little more than a month ago, I listed three pressing Obamacare questions that had yet to be answered. One one was the creme de la creme of questions: What percentage of paying enrollees are healthy young adults? On Monday, the HHS released this first bit of this "Holy Grail of data," and the initial results (links opens PDF) weren't too encouraging on the surface.

Despite enrollment surging to 2.15 million, just 24% of all enrollees (489,460) are in the 18 to 34 year age range, while a whopping 79% of enrollees received some form of financial assistance.

In addition, we discovered that 80% of enrollees selected one of the two lower-tiered plans, bronze (20%) or silver (60%), with few people opting for more expensive but lower deductible gold (13%) or platinum (7%) plans. Furthermore, the 20,224 catastrophic plan enrollments means very few people took advantage of the ability to extend catastrophic plan coverage in 2014 that would have otherwise been cancelled under the expanded benefits deemed necessary for insurers by the PPACA. If you recall, there were nearly 6 million people poised to lose their health insurance on Jan. 1 according to Forbes, so it appears that few people took advantage of the Obama Administration's attempt to extend coverage without these citizens having to face a significant increase in premium prices.

Does this mean Obamacare is destined to fail?

These results demonstrate a significant shortfall in the number of young adult signups, which the HHS had pegged at 38% of the 7 million enrollees before the health exchanges opened for business. This is a problem because healthier young adults are needed by insurers to help offset the costs of treating elderly and terminally ill patients, especially because a major new component of the PPACA is that insurers can't turn down people with preexisting conditions. As I've noted before, half of all health expenditures in this country are spent on just 5% of the population annually, so healthier adults are needed to help allay these disproportionate costs.

Monday's initial data would imply that this ongoing young adult enrollment shortfall will necessitate significant premium price hikes by insurers for 2015 to help offset the costs of treating sick patients, calling into question the whole premise that a more universal health reform, which brought more paying Americans into the fold, would help reduce long-term costs.

The addition of roughly 4 million Medicaid-approved members further complicates the burden of expanding health insurance under Obamacare relative to just 2.15 million paying sign-ups.

Not so fast...

While the data thus far would indeed portend bad news for future premium pricing, there isn't enough reason for consumers or investors to start running for the hills... yet!

The first factor to consider is that we still have two-and-a-half months of eligible enrollment left before Obamacare's 2014 coverage cutoff period ends. Americans are notorious procrastinators when it comes to paying their bills, so it would come as no surprise if we saw the bulk of enrollments on the back end of the coverage cutoff date.

With that being said, perhaps no age group procrastinates more than young adults. I should know – I am one, and I can tell you firsthand that quite a few of my friends in that age range are still pondering what they're going to do with regard to purchasing health insurance for themselves.

In addition, I wouldn't be too alarmed for insurers that a majority of Americans are choosing the cheaper path by purchasing bronze and silver plans relative to gold and platinum plans. In fact, insurers and the HHS were dead on in their estimation that silver plans would be the most popular choice among potential customers. Similar to a retail environment, lower priced products can often have the beefiest margin potential, especially for insurers, which will rely on consumers to kick in 30% to 40% of the medical costs as well as co-pays.

Specifically, I would say this benefits a company like WellPoint (NYSE: WLP ) , which purchased Amerigroup for $4.5 billion to focus on government-sponsored individuals. WellPoint, which has a strong presence in California and New York, should see benefits from Medicaid enrollments, as well as some of the 2.15 million paying enrollees.

Worry about this instead

Instead of worrying about the shortfall in young adult signups that could very well be rectified by late March, I would instead be concerned for hospital providers and pricier medical device makers, which may have something to worry about with the number of bronze and silver plans coming in at 80% combined.

Whereas this figure works in the favor of insurers, hospitals run the risk of patients simply being unable to pay for services rendered. Although out-of-pocket costs are about the same for all insurance tiers, the percentage of payment due for services rendered is considerably higher for bronze and silver plans. Let's face it -- the reason consumers selected these plans likely had a lot to do with costs, so when they do eventually require medical care, it could be an adventure to see if these hospital providers can collect. An operator I worry about is Tenet Healthcare (NYSE: THC ) given that a number of its hospitals are in regions of the country where Medicaid isn't expanding, leaving an already disproportionate number of uninsured people still uninsured.

This is also a concern for medical device makers like Intuitive Surgical (NASDAQ: ISRG ) . In spite of Intuitive's solid preliminary revenue guidance for the fourth quarter, the uncertainties surrounding Obamacare's implementation have caused many health-sector companies to hold back on their spending. With Intuitive's soft tissue surgical system known as da Vinci costing roughly $1.5 million, it may find the sales environment difficult for the time being. Yesterday's preliminary report, though better than Wall Street expected, did show a marked 23% decline in surgical system sales, which I believe could be a direct result of Obamacare and hospital's cautionary spending habits.

We're almost there

With three-and-a-half months of enrollment in the books, we're more than halfway to the March 31 coverage cutoff date. While the initial data looks disappointing in terms of young adult sign-ups, I'd feign to call Obamacare a failure as of yet – though it will need to work hard to lure in young adults from this point forward. As we approach and pass March 31, we'll have a considerably better idea of how successful Obamacare was in luring young adults to purchase health insurance, and what the future might hold for insurance premiums in 2015.

Re: Who's Sorry Now?

Good article oldr; lots of actual information...

I stand corrected on the point about HHS not releasing the number on the "young and healthy" ; apparently they finally did that this week...

And it's easy to see why it took so long; they still need about a 50% increase in the percentage to be on target. (But frankly it's higher than I personally thought it would be running.)

And of course we still need the breakdown on paid versus non-paid for any of the numbers being reported to have real meaning...

A category of folks who's ranks will balloon many times over if the CBO targets aren't met and premiums and deductibles spike...

And of course we still need to see what the impact of the employer mandates will be...

Yeah, just a tad early to be dancing in the end zone and dumping water on the coach...

For anyone but blind shills, anyway...

I stand corrected on the point about HHS not releasing the number on the "young and healthy" ; apparently they finally did that this week...

And it's easy to see why it took so long; they still need about a 50% increase in the percentage to be on target. (But frankly it's higher than I personally thought it would be running.)

And of course we still need the breakdown on paid versus non-paid for any of the numbers being reported to have real meaning...

And let's not forget the Jessica Sanfords who have lost their existing plans, and can't afford the new ones, who will now be joining the "emergency room as primary care" group...a whopping 79% of enrollees received some form of financial assistance.

A category of folks who's ranks will balloon many times over if the CBO targets aren't met and premiums and deductibles spike...

And of course we still need to see what the impact of the employer mandates will be...

Yeah, just a tad early to be dancing in the end zone and dumping water on the coach...

For anyone but blind shills, anyway...

Last edited by Lord Jim on Fri Jan 17, 2014 12:24 am, edited 1 time in total.

Re: Who's Sorry Now?

Okay... There's all kinds of things wrong with what you just said.

Re: Who's Sorry Now?

That's interesting CP...

I listen to a lot of MSNBC while I'm working, and I read the NY Times every day, and this is the first I've heard about this...(obviously, or I wouldn't have made the reference; unlike somebody around here I'm not the sort to repeatedly make reference to something that I know has been proven false. I'm not in the shilling and dissembling business.)

I would have thought that those two media outlets would have been trumpeting this story...(maybe I missed it because it broke right before Thanksgiving and I wasn't paying as much attention to the news as I usually do.)

I listen to a lot of MSNBC while I'm working, and I read the NY Times every day, and this is the first I've heard about this...(obviously, or I wouldn't have made the reference; unlike somebody around here I'm not the sort to repeatedly make reference to something that I know has been proven false. I'm not in the shilling and dissembling business.)

I would have thought that those two media outlets would have been trumpeting this story...(maybe I missed it because it broke right before Thanksgiving and I wasn't paying as much attention to the news as I usually do.)

Re: Who's Sorry Now?

I wouldn't have known except for a news story I heard yesterday about how most of these horror stories are at the very least misinformed if not out and out lies that drove me to do a web search.

I am reminded of your sig line at the last version of the CSB

I am reminded of your sig line at the last version of the CSB

Okay... There's all kinds of things wrong with what you just said.

-

oldr_n_wsr

- Posts: 10838

- Joined: Sun Apr 18, 2010 1:59 am

Re: Who's Sorry Now?

Thanks LJ. I have found myself looking in "other places" for info about the obamacare. most/all of the common info out there is from sources on either side of no mans land.Good article oldr; lots of actual information...

The link I gave is to Motely Fool who's only dog in the race is how the ACA pertains to investing. It does not have an agendaand only cares about how it's affecting the marketplace. If you click on the link and look at the very bottom, they disclose anything they may have investments in if htey mention them in the article. they really only want info so they can make intelligent investment choices regardless of whether or not the ACA is a success.

Re: Who's Sorry Now?

A few years ago, one Rush H. Limbaugh III was excoriated for saying on his syndicated radio program that he "wanted Obama to fail."

What a racist, un-American, partisan bastard was he.

But this is exactly what he was talking about. Obama was "successful" in getting this abomination passed. Success. And now 80% of the American working population who already had satisfactory healthcare coverage will have either (1) the same coverage at a much higher cost, or (2) significantly worse and less inclusive coverage (i.e., higher deductibles and co-pays) at the same cost as before. I am in the latter group. My annual out-of-pocket will go from about $1,000 to about $4,000.

If Obamacare is "successful," tens of millions of young, healthy Americans will be compelled to purchase insurance that they do not need, to supplement the premiums of millions of old farts (like me) who will - at least in theory - get more coverage than they actually pay for.

And we will all be paying for numerous coverages that we don't want or need (birth control?), because Barry & The Progressives think it's a good idea for everyone to have them.

Dimwit rubato seeks to use fairytale statistics to prove that O'care is successful in signing up - as I said - millions of young, healthy people who don't actually require coverage. If this is how you measure success, you are welcome to it. It is bullshit.

What a racist, un-American, partisan bastard was he.

But this is exactly what he was talking about. Obama was "successful" in getting this abomination passed. Success. And now 80% of the American working population who already had satisfactory healthcare coverage will have either (1) the same coverage at a much higher cost, or (2) significantly worse and less inclusive coverage (i.e., higher deductibles and co-pays) at the same cost as before. I am in the latter group. My annual out-of-pocket will go from about $1,000 to about $4,000.

If Obamacare is "successful," tens of millions of young, healthy Americans will be compelled to purchase insurance that they do not need, to supplement the premiums of millions of old farts (like me) who will - at least in theory - get more coverage than they actually pay for.

And we will all be paying for numerous coverages that we don't want or need (birth control?), because Barry & The Progressives think it's a good idea for everyone to have them.

Dimwit rubato seeks to use fairytale statistics to prove that O'care is successful in signing up - as I said - millions of young, healthy people who don't actually require coverage. If this is how you measure success, you are welcome to it. It is bullshit.

Re: Who's Sorry Now?

http://delong.typepad.com/sdj/2014/01/o ... trina.html

LOL!

yrs,

rubato

Obama's Katrina!!

We're now at the point in "Obama's Katrina" when the number of uninsured people in West Virginia has been reduced by a third.

— LOLGOP (@LOLGOP) January 21, 2014

LOL!

yrs,

rubato

Re: Who's Sorry Now?

http://acasignups.net/

LOLGOP!

yrs,

rubato

Private QHPs: 2.53M •

Medicaid/CHIP: 6.32M •

Sub26ers: 3.1M

Total as of Jan 21, 2014: 11.95 Million

Enrollment Period Elapsed: 61.5% •

CBO Projection Attained: 35.9%

1.2 million New medicaid enrollments just in California.Submitted by Charles Gaba on Tue, 01/21/2014 - 8:19pm

Source:

The Fresno Bee, 01/17/14

Hat Tip To:

Ruth 37

When I posted my big Medicaid/CHIP spreadsheet overhaul, I was understandably concerned that I missed something major--that there had to be some factor lost in the messy, semi-overlapping reports from HHS and CMS that would account for big swaths of the 1.7 million "extra" Medicaid enrollments that I've "found" (in reality, those 1.7 million have been gradually accruing ever since the beginning of October, I just wasn't able to pin them down into a tangible format on the spreadsheet & graph until now). As a case in point, after the overhaul, I have California sitting at 1.214 million new additions to Medicaid/CHIP programs.

Today a friend provided a link to a story out of the Fresno Bee from 4 days ago, in which the Cailifornia Dept. of Health Care Services reveals that enrollments in Medi-Cal (CA's implementation of Medicaid) have gone up from 8 million people last year up to about 9.2 million as of now...a difference of about 1.2 million.

I'm not saying that there aren't flaws in my methodology; no doubt there are, but this certainly helps set my mind more at ease.

"Medi-Cal is huge. In previous columns, I described it as serving more than 8 million Californians. That was so 2013. Under Obamacare, Medi-Cal broadened its eligibility on Jan. 1, opening the program to more Californians, including childless adults, who previously were ineligible.

"How many people have enrolled so far under the expansion? The state Department of Health Care Services, which administers Medi-Cal, hasn't been terribly forthcoming with the answer. But it did say this when I asked: "Curre

LOLGOP!

yrs,

rubato

Re: Who's Sorry Now?

http://delong.typepad.com/sdj/2014/01/m ... .html#more

The idiots are actively trying to prevent people from getting health care!

yrs,

rubato

Massive Resistance Watch: The View from The Roasterie LXXXI: January 23, 2014

Fifty years from now which will play worse in historical memory: the conservative southern Democrats' (all Republicans today) massive resistance to try to civil rights in the 1950s and the 1960s or the conservative Republicans' massive resistance to their poorer fellow-citizens getting health insurance in the 2010s?

I cannot tell. I do, however, think that history will judge the second as stupider: practically everyone has somebody uninsured or at risk of rapidly becoming uninsured in their extended family, and throwing federal Medicaid and exchange subsidy dollars down the toilet does run a measurable risk--10%? 20%? 50%?--of send the red state economies as a group back into recession over the next two years.

But things aren't all going their way. Sy Mukherjee reports:

Sy Mukherjee: Federal Judge Temporarily Blocks Missouri's Restrictions On Obamacare Navigators: "Obamacare uses so-called state navigators and enrollment counselors to assist Americans who are looking to buy health plans....

Although navigators have to be federally certified, the health law allows states to impose additional requirements.... 19 states generally opposed to the Affordable Care Act have passed such laws--and some states’ navigator requirements are so stringent that advocates say they prevent counselors from fulfilling their very purpose.... Missouri’s navigator law... prohibits federally certified navigators from discussing specific marketplace plans unless they also become state-licensed insurance brokers.... “Missouri has placed groups like St. Louis Effort for AIDS in an untenable situation,” said plaintiff’s counsel and former Missouri insurance commissioner Jay Angoff when he filed the lawsuit last winter....

Judge Ortrie Smith agreed... concludes HIMIA’s requirement that federally approved/licensed individuals and entities must also comply with additional licensing requirements constitutes an impermissible obstacle.... “[T]he suggestion that those designated to operate the [Obamacare marketplace] can do so only if they are also licensed as insurance agents demonstrates that the state law obstructs the federal purpose.”

A federal judge in Tennessee temporarily blocked a similar law in that state in October...

The idiots are actively trying to prevent people from getting health care!

yrs,

rubato