Some answers to the rhetorical question would have been helpful.

What, if any, approximations of Fannie/Freddie/CRA/GSE did any of those countries have? If they existed, how closely did they resemble ours? What actions did they take which ours did not? What actions did ours take that theirs did not?

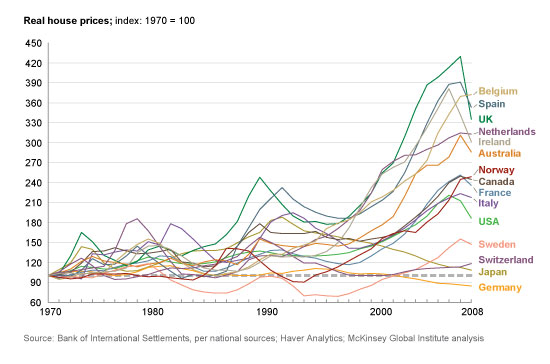

And among the countries other than the US, why did Germany, Japan, and Switzerland not have mid-to-late-2000s housing-price bubbles while Spain and the UK did?

Graphical presentations of evidence are valuable tools. But they do not, in themselves, necessarily explain the evidence which they depict.

Reason is valuable only when it performs against the wordless physical background of the universe.

"...

If one truly thinks the “Crash” was all Fannie and Freddie’s fault, then one must explain how nearly every other industrialized nation at the same time experienced the same basic arc of a housing boom and bust… when the other nations did not have Fannie or Freddie with which to contend?

Take note of the exceptions: Germany never followed US fiscal or monetary (that’s EU/ECB territory) or deregulatory policies. Independent Switzerland never follows anyone’s policies and is not part of the EU/ECB. And, Japan had already experienced it’s housing bubble a decade earlier. Other than that, the balance did not have US policies supposedly encouraging sub-prime lending through Fannie or Freddie, but they did have other policies and actions in common with the U.S, and we will explore those toward the end.

... "

"...

“Doesn’t-Matter-What-Is-Your-Ideology” Explanation For Housing & Financial Market Collapse

So what are the facts; what is the reality field? The US economy is quite complex and intricate, so certainly, no single problem or matter was the cause. But, to be sure, there is a cause.

Check it out:

● Former Federal Reserve Chair Alan Greenspan reduced rates to 1 percent — lowest in 50 years — and kept them there for a uniquely long time…

● Low rates led to lower general yields on municipal bonds or Treasurys. Fund managers then turned to high-yield mortgage-backed securities — failing to do adequate due diligence before buying them.

● Fund managers made this error and relied on credit ratings agencies to do their work — Moody’s, S&P and Fitch. But, the ratings agencies had placed AAA ratings on junk securities, claiming they were as safe as U.S. Treasurys.

● Derivatives became an unregulated financial instrument hiding the truth of real risk. Exempt from proper oversight, insurance supervision, and reserve requirements, derivatives permitted AIG to write $3 trillion in instruments while reserving absolutely nothing against future claims.

● The Securities and Exchange Commission changed the leverage rules for the exclusive pleasure of five Wall Street banks in 2004. The “Bear Stearns exemption” replaced the previous capitalization rule leverage limit and permitted unlimited leverage for Goldman Sachs, Morgan Stanley, Merrill Lynch, Lehman Brothers and Bear Stearns.

● Wall Street’s compensation system encouraged a short-term performance perspective, and offered traders great upside with none of the downside, leading to excessive risk-taking.

● The demand for higher-yields led Wall Street to begin bundling mortgages, with the highest yields coming from subprime mortgages cleverly buried in piles with prime mortgages. This deceptive market for packaging mortgage-backed instruments was exempt from most regulations. The Federal Reserve could and should have provided oversight, but Greenspan chose not to… ever the Ayn Rand free marketeer.

● The mortgage originators’ unregulated scheme saw them holding mortgages for a very short period, thus allowing them to be creative/unscrupulous with underwriting standards, ignoring all traditional lending metrics such as income, credit rating, debt-service history and loan-to-value.

● New mortgage products came on the market to attract more subprime borrowers to create higher yielding packaged instruments — adjustable-rate mortgages, interest-only, piggy-back mortgages (concurrent mortgage and home-equity line) and negative amortization loans (borrower’s indebtedness goes up each month). These “innovative” private-sector mortgages — not those encouraged by HUD policies — defaulted in hugely disproportionate frequency compared to traditional 30-year fixed mortgages.

● To remain competitive and satisfy demanding boards and shareholders, traditional banks developed computerized underwriting systems for mortgages and relied on software programs instead of thoughtful managers. Employees were paid on loan volume, not quality.

● The Glass-Steagall Act — previously the fire wall separating Wall Street investment banks and Main Street commercial banks — was repealed in 1999 during our deregulatory zeal, thus allowing FDIC-insured banks (deposits guaranteed by the government) to enter into excessively risky business arrangements. The law’s repeal also permitted industry consolidation to the extreme.

● In 2004, the Office of the Comptroller of the Currency preempted state laws regulating mortgage credit and national banks. Thereafter, national lenders sold increasingly risky mortgage products in those states. Then… default and foreclosure rates skyrocketed.

Deregulating the financial sector, jettisoning protections that had succeeded for decades is THE FATAL FLAW.

Congress failed its obligation and permitted Wall Street to self-regulate, and Greenspan through the Fed ignored financial market abuses, falling prey to his own coined phrase of “irrational exuberance.” His exuberance was his belief in the purity of free markets.

The discredited belief that free markets require no adult supervision is the reason for our crisis and why a new false narrative has been created.

... "

dgs49 wrote:Government regulators didn't "encourage" banks to issue risky mortgage loans to unqualified borrowers?

No. Nothing in the CRA or any other legislation obligated banks to issue loans to unqualified borrowers. Banks did that all on their own because they saw there was money to be made in doing so. Period. And please spare us the references to borrowers who were below average income or who bought houses below average price. Neither of those equate to "risky" or "unqualified".

Fannie Mae and Freddie Mac didn't buy the paper?

Fannie Mae and Freddie Mac had an insignificant exposure to subprime mortgages (something like $160 billion out of a $9 trillion portfolio). Even if they had to write off all of it, it would have barely caused a blip.

"When a man has so far corrupted and prostituted the chastity of his mind, as to subscribe his professional belief to things he does not believe, he has prepared himself for the commission of every other crime."

Scooter wrote:]Fannie Mae and Freddie Mac had an insignificant exposure to subprime mortgages (something like $160 billion out of a $9 trillion portfolio). Even if they had to write off all of it, it would have barely caused a blip.

As has been shownb previously, mae/mac held the lions share of ALL US mortgages. Their demise was unstoppable trigger effect. This is old news, why is it still being discussed here? The govt, slow as it is, has moved onto the indictment phase.

(and of course we still gloss over the fact that mae/mac were prevented by their GSE charter from holding ANY of the paper....)

You really do have to read to understand the facts.

The percentage of all loans underwritten by Fannie and Freddie was falling during the boom, from over 50% to about 37%. The difference was being taken up by the unregulated private mortgage-backed securities who were buying nearly ALL of the bad paper.

We also know this is true because the chart in the first post proves it. All of the countries which had a crash had relaxed lending rules and saw a boom in private-mortgage backed securities.

If you consider the facts the conclusion is obvious that any contribution of Fannie and Freddie was inconsequential.

The boom was driven be deregulation and other factors outlined above.

rubato wrote:You really do have to read to understand the facts.

This is true. in 2008 when the bust occured, it was about 50% of all mortgages and valued at over $600b in subprime.

there are many factors true, factors that I have posted before and apparently you neglected to read or retain. I dont see the value add in doing it again.

Suffice to say, you are the only person in the US that disattribute any affect by mae/mac. that lack of reasoning boggles. but nevertheless, the associated lending in some areas of the US approached *90* percent, as opposed to the overall 20% nationwide. those areas will never recover.

(ps - you also need to realize that the overall 20% price decline in the US affected *ALL* mortgage backed securities which was almost $7.5T in the same timeframe.